Tracey Emin: Market Structure and Visibility Cycles Ahead of A Second Life at Tate Modern

A Second Life at Tate Modern reads unmistakably as a Lazarus story. The exhibition traces Tracey Emin’s career from rupture and provocation to survival and renewed conviction. Spanning four decades and culminating in monumental bronzes and expansive paintings, it consolidates Emin’s position within the canon while presenting her recent work as a phase of material and emotional authority. While the curatorial narrative evokes rebirth, her secondary market reflects a mature structure in which visibility concentrates liquidity more readily than it resets value. The question for collectors is how that dynamic unfolds when canon becomes cemented.

→ Explore Tracey Emin's Market Intelligence Dashboard

Tracey Emin’s forthcoming exhibition at Tate Modern occurs against an established, segmented, and cyclical market that has historically moved in visibility-driven cycles. Over the past decade, her auction performance has followed phases of compression and selective rebound, often shaped by the composition and calibre of works entering the market.

Indexed analysis shows that Emin’s pricing cycles display greater amplitude than the broader Post-War sector, with deeper corrections and recoveries clustering around moments of concentrated attention. Repricing has been episodic and clustered in high-quality unique works.

The forthcoming Tate Modern exhibition is therefore likely to compress competition within the upper tier during the exhibition period. Institutional visibility historically concentrates attention on a narrow group of works, particularly major paintings and sculpture, where collectors respond most directly to curatorial framing.

To explore this dynamic in practice, Artscapy will host a private collector visit to A Second Life at Tate Modern, with a curator-led tour highlighting key works across Emin’s career, including several on public view for the first time.

→ Join Artscapy collector events

This exhibition is taking place against a broader post-2022 contraction in global auction liquidity, making absorption capacity more consequential than narrative momentum alone. Therefore, collectors should approach the exhibition as a timing-driven phase within a market whose underlying mechanics remain intact.

The market context

Tracey Emin’s secondary market is best understood as mature but episodic. Pricing has moved in cycles, with periods of sharp contraction followed by selective rebound. These movements intersect with broader macroeconomic conditions but are not fully explained by them, indicating that artist-specific dynamics play a meaningful role in shaping outcomes.

3.1 Median hammer price index: Tracey Emin vs post-war & contemporary market

Source: Artscapy | Visualisation: Darden Gildea

→ Explore the data behind this chart (must be a member & logged in)

The indexed comparison makes the relative volatility clear. From 2019 through 2022, Emin’s median price index declined materially more than the broader Post-War benchmark, underscoring deeper contraction during periods of macro softness. The subsequent 2024 rebound was equally pronounced, with pricing recovering more abruptly than the sector average and clustering around a discrete visibility event.

This pattern suggests a market that amplifies broader cycles rather than escaping them. When conditions soften, median prices compress more quickly; when attention intensifies, recovery accelerates. The magnitude of these swings indicates sensitivity to the composition and quality of works entering the market, as well as to exhibition-driven attention.

Importantly, the divergence is episodic rather than structural. Over the full period, Emin’s index does not decouple from the broader market; it moves within it, but with greater amplitude. The 2024 inflection, coinciding with I followed you to the end at White Cube, illustrates how concentrated visibility can compress recovery into a short window without permanently resetting baseline valuations.

3.2 Sell-through rate over time

Source: Artscapy | Visualisation: Darden Gildea

Liquidity data provides an important counterpoint to this price volatility. While median prices compressed sharply in 2022 and rebounded thereafter, sell-through rates declined more moderately, bottoming out around 80% before recovering. Sell-through rates softened, but remained within normal auction levels, indicating a decrease in market demand.

This divergence between price movement and participation suggests that the contraction phase was driven more by valuation adjustment and selective bidding than by a collapse in demand. Buyers continued to transact, albeit with greater discipline, and competition concentrated around higher-quality works.

Taken together, the data indicates continued demand but an increase in sensitivity to the quality and timing of lots supplied; therefore, prices adjust quickly in response to the increased visibility and change in consignment composition, while buyer's demand moderates more gradually. This asymmetry shapes how institutional catalysts are likely to shape near-term market conditions.

3.3 Relative positioning and volatility trajectory

Source: Artscapy | Visualisation: Darden Gildea

Source: Artscapy | Visualisation: Darden Gildea

To contextualise Emin’s trajectory, it is helpful to compare her indexed median performance with that of Cecily Brown and Rachel Whiteread, peers whose markets have evolved along structurally distinct paths. This indexed comparison reveals three differentiated patterns.

Cecily Brown’s market demonstrates the clearest structural rerating. While cyclical contractions occur, recoveries sit within a broader upward arc. Greater annual turnover reduces compositional distortion, and deeper international participation supports steadier long-term progression.

Rachel Whiteread’s index exhibits sharper year-to-year swings. These movements are largely attributable to thinner annual lot counts and medium concentration. With fewer works transacting annually, shifts in supply composition exert a disproportionate influence on median outcomes. Volatility in this context reflects supply sensitivity rather than systemic repricing.

Emin occupies an intermediate position. Her pricing cycles show greater amplitude than Brown’s steadier ascent, yet her volatility is less structurally supply-driven than Whiteread’s. Contractions have been pronounced, but recoveries cluster around visibility events rather than reflecting sustained baseline escalation. The 2022–2024 sequence, compression followed by catalyst-linked rebound, underscores a market that is institutionally embedded yet highly attention-responsive.

This relative positioning suggests embedded elasticity rather than fragility. Emin’s market has not transitioned into the lower-variance profile characteristic of fully consolidated blue-chip peers, nor does it resemble a thin market governed primarily by irregular supply. Instead, pricing momentum remains closely tied to exhibition cycles and consignment quality.

The forthcoming retrospective may influence how this elasticity is interpreted. As Artscapy’s Chief Sales Officer Daniela Bianco observes, the exhibition “positions Emin’s work as contributing to ongoing discussions around identity, the female body in art, and autobiographical vulnerability as a valid and powerful artistic strategy, a shift from the tabloid focus that marked her early career.” A sustained reframing from notoriety to formal authority could affect how collectors assess late-period works within the existing hierarchy.

Historical precedent, however, indicates that narrative recalibration alone does not guarantee structural rerating. Durable uplift within this peer cohort has typically required expanded buyer depth or sustained upper-tier supply constraint rather than institutional recognition in isolation.

Case study: I followed you to the end at White Cube

The 2024 I followed you to the end exhibition at White Cube offers a contained environment to test how Emin’s market responds to concentrated commercial visibility. Whereas institutional retrospectives consolidate reputation over longer horizons, commercial exhibitions operate within compressed timelines, shaping consignor behaviour, buyer urgency and pricing expectations more immediately.

4.1 Median hammer price by visibility phase

Source: Artscapy | Visualisation: Darden Gildea

Segmenting transaction data across pre-exhibition, lead-up, exhibition, and post-exhibition phases reveals differentiated transmission across market tiers rather than uniform repricing.

Source: Artscapy | Visualisation: Darden Gildea

For paintings, neons, and sculpture, the mediums most prominently featured in I followed you to the end, median values expanded sharply during the exhibition window. The exhibition phase contains materially fewer transactions (n=12), indicating that the median reflects a concentrated cluster of higher-value consignments encountering intensified bidding rather than broad-based repricing across the secondary market. Demand compressed around a limited number of significant works, concentrating pricing momentum at the top of the market. After the exhibition, median prices moderated toward earlier ranges, reinforcing that the expansion was tied to the visibility window rather than a structural shift in baseline valuation.

Source: Artscapy | Visualisation: Darden Gildea

Source: Artscapy | Visualisation: Darden Gildea

Prints and multiples followed a different sequencing pattern. Median values rose during the anticipatory lead-up phase, albeit on thin volume, but did not sustain comparable expansion during the exhibition itself. The exhibition window for prints contains minimal transactional activity, and pricing did not extend meaningfully beyond pre-visibility levels. This pattern suggests early positioning rather than sustained competitive escalation.

Taken together, the segmentation indicates that visibility transmits asymmetrically. Competitive intensity peaks in scarce, institutionally aligned works during concentrated attention, while lower-tier segments display continuity rather than repricing. The exhibition window therefore concentrates liquidity in upper tiers rather than elevating pricing uniformly across mediums.

4.2 Coefficient of variation: a measure of volatility

Source: Artscapy | Visualisation: Darden Gildea

Volatility data shifts the focus from sequencing to structure. The coefficient of variation, calculated as the standard deviation divided by the mean, measures relative price dispersion within each period. This metric widened materially during periods of stress and concentrated visibility. The most pronounced expansion occurred in 2022, when median pricing compressed sharply while a limited number of higher-value works continued to transact at elevated levels. The result was a widening spread between peak realisations and the broader transaction base.

The spike in dispersion reflects tier bifurcation rather than instability. Incremental demand did not disappear; it concentrated in a narrow band of high-quality, institutionally aligned works. As visibility intensified, additional capital competed for scarce upper-tier material, stretching top-end pricing without proportionately lifting broader segments. Participation in lower tiers remained comparatively steady, but pricing momentum was unevenly distributed.

This dynamic was visible again during the exhibition window, when Emin’s painting This is life without you – You made me Feel like This (2018) achieved £899,000 against a pre-sale estimate of £600,000 to £800,000 at Phillips in October 2024. The result exceeded the high estimate by 11.1% and materially surpassed comparable works auctioned in the preceding quarter. Its scale and alignment with the exhibition narrative positioned it squarely within the upper tier that absorbed intensified bidding pressure.

In contrast, the print True Love Always Wins, offered at Phillips in the same season, realised £3,814 against a £3,000 to £4,000 estimate, clearing within range but without competitive extension. The divergence within the same venue and cycle underscores how incremental demand concentrated in unique, high-value works rather than diffusing across the broader market.

4.3 Lot volume over time

Source: Artscapy | Visualisation: Darden Gildea

Transaction volume during the period underscores that pricing inflections were driven by composition rather than aggregate supply growth. The 2022–2023 expansion in lot count coincided with median hammer price compression, demonstrating that increased volume alone does not elevate pricing in a mature market.

The White Cube exhibition window marked a different dynamic. During the months corresponding to the show, five neon works appeared at auction in the U.K., compared to two in the same period a year prior. The clustering of a prominently featured medium indicates strategic consignment timing, with owners bringing institutionally aligned works to market under heightened visibility.

Median expansion during this phase therefore reflected selective supply meeting concentrated demand. When scarce, high-calibre works enter the market at moments of intensified attention, pricing can stretch at the upper tier even without broad-based demand expansion. The effect is compositional, not structural.

As the visibility window closed and supply broadened in subsequent months, median levels moderated. The episode demonstrates that exhibition cycles shape not only bidding intensity but also the quality and timing of works entering the market, reinforcing the market’s sensitivity to composition rather than volume.

Medium differentiation

While the White Cube cycle illustrates how visibility transmits across tiers in real time, revenue composition reveals the longer-term structure of Emin’s market.

5.1 Gross hammer revenue by medium

Source: Artscapy | Visualisation: Darden Gildea

Revenue distribution reveals a clear value hierarchy. Paintings account for the majority of total hammer value across peak years, with mixed-media and sculpture contributing episodically but at materially lower aggregate levels. Prints and multiples represent a substantial share of transaction volume yet comprise a comparatively modest portion of total revenue.

This asymmetry reflects a pyramidal market structure in which capitalisation is concentrated in a limited number of high-value works. Revenue expansion has been driven by upper-tier consignments rather than broad-based medium appreciation. Aggregate capitalisation therefore fluctuates in accordance with the release and competitive absorption of high-value paintings, while lower tiers provide continuity in liquidity without materially altering total value concentration. Across cycles, total revenue expansion has been painting-led, reinforcing that medium-based concentration is a persistent structural feature of the market rather than a temporary by-product of visibility events.

5.2 Median price by medium

Median pricing further distinguishes the tiers. Unique works, particularly paintings, neons, and major sculpture, operate at materially higher price bands and exhibit greater amplitude during visibility cycles, driving index movements and headline results. Editioned works transact consistently but within narrower pricing bands. Their role is absorptive rather than expansive, providing continuity without materially shifting total value distribution.

Taken together, the medium data indicate that pricing momentum in Emin’s market originates at the top of the value ladder. Visibility events may broaden participation, yet historical expansion in aggregate value has concentrated in institutionally aligned works.

The Tate exhibition reinforces this hierarchy. As Daniela Bianco observes, it “positions Emin’s work as contributing to ongoing discussions around identity, the female body in art, and autobiographical vulnerability as a valid and powerful artistic strategy — a shift from the tabloid focus that marked her early career.” This reframing directly affects the upper tier. If institutional emphasis continues to privilege formal evolution and scale, late paintings and major works may command increased relative attention within an already capital-concentrated structure.

For collectors, the implication is strategic rather than tactical. Exposure to dominant capital tiers offers greater sensitivity to visibility-driven momentum, whereas lower tiers provide liquidity without equivalent leverage to repricing cycles.

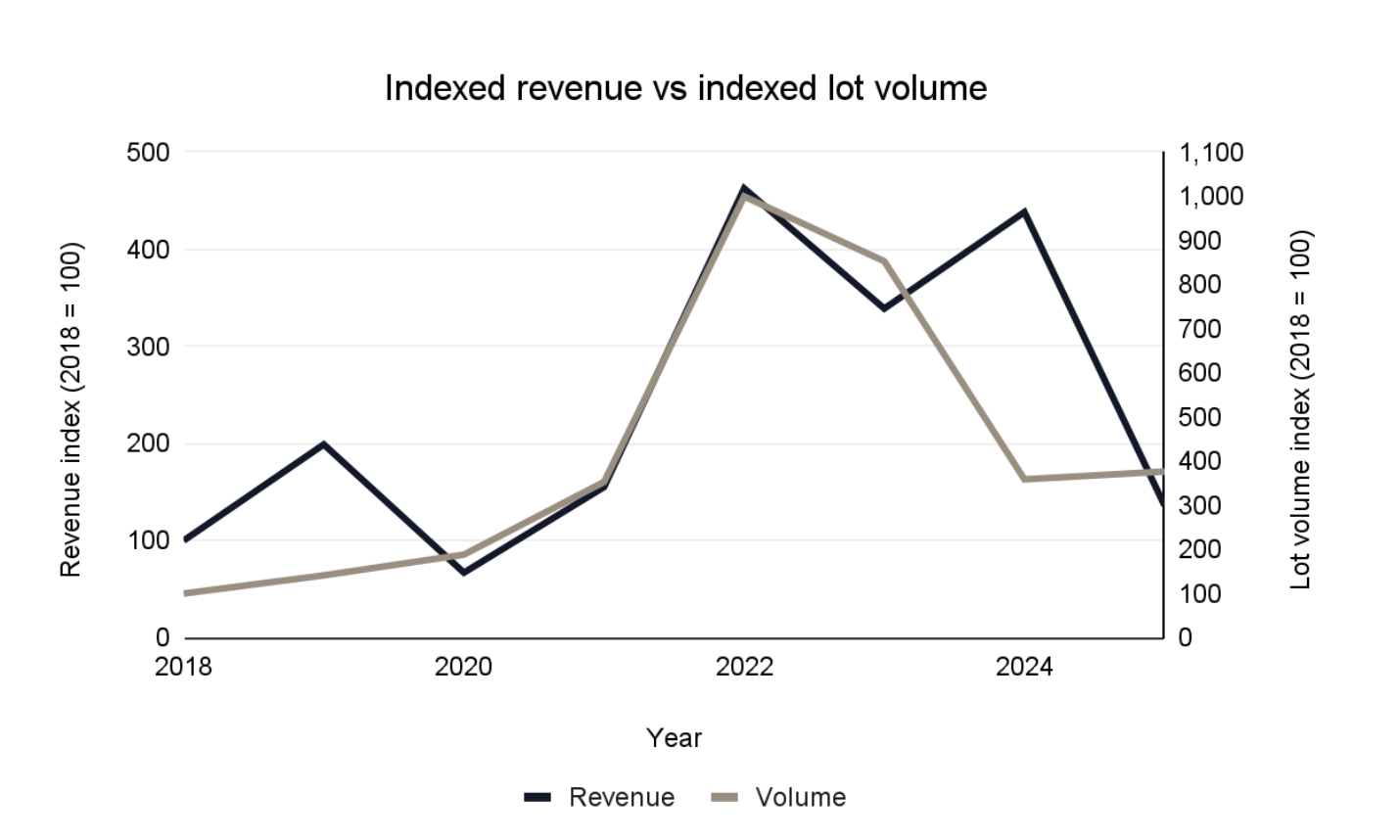

Supply Sensitivity and Market Depth

Source: Artscapy | Visualisation: Darden Gildea

The relationship between indexed revenue and indexed lot volume clarifies the limits of market depth within Emin’s secondary market. While transaction counts have expanded across several cycles, aggregate revenue has not advanced proportionally at higher pricing baselines. Increased volume, in other words, has not consistently translated into structural price elevation.

Revenue inflections tend to coincide with the entry of selectively strong consignments rather than broad-based participation across tiers. When higher-calibre works cluster within a given season, total revenue rises even if median pricing across the wider market remains stable or compresses. Conversely, periods marked by expanding lot counts without a comparable increase in quality have corresponded with median softening or widened dispersion.

This pattern indicates finite absorption capacity. Buyer participation remains durable, but incremental demand is concentrated within the upper tier. When supply expands beyond that band of high-quality demand, pricing pressure emerges first within mid-level segments before reaching the top of the market.

Compared with artists supported by broader international demand, where incremental supply can enter without immediate compression, Emin’s revenue-volume relationship appears steeper. Marginal supply encounters demand constraints more quickly, reinforcing tier concentration and limited elasticity at mid-range price levels.

In the context of heightened visibility, particularly around institutional exhibitions, this interaction becomes critical. If additional consignments enter the market alongside intensified competition, outcomes will hinge on the distribution of demand across tiers rather than headline momentum alone. Volume expansion without proportional depth risks redistribution of value rather than structural uplift.

Geographic structure: concentration and international reach

Emin’s secondary market exhibits pronounced geographic concentration, with the United Kingdom functioning as its primary demand base and pricing venue. While transactions occur in New York, Europe, and Hong Kong, value realisation and liquidity consistency remain anchored in London.

7.1 Geographic concentration of capital

Source: Artscapy | Visualisation: Darden Gildea

Revenue distribution and transaction frequency indicate that Emin’s secondary market is structurally anchored in the United Kingdom. The U.K. has recorded sales in every observed year, whereas other regions exhibit more sporadic activity, with clusters of high-value works appearing in isolated cycles rather than sustained participation. Although high-value consignments occasionally concentrate in the United States or Asia, international engagement has not demonstrated the same continuity of transaction flow.

This pattern suggests that geographic expansion remains conditional rather than foundational. The U.K. provides the market’s most stable base of liquidity, while international participation tends to intensify during favorable cycles or around moments of heightened visibility before moderating. In this context, pricing impulses that emerge during exhibition windows are more likely to reinforce domestic demand dynamics than to signal durable geographic broadening.

Relative to peers such as Cecily Brown, whose auction market reflects deeper and more continuous U.S. participation, Emin’s demand structure remains more domestically concentrated. Brown’s pricing power is supported by broader cross-border capital, whereas Emin’s market exhibits greater dependence on U.K.-based absorption, with international bidding functioning as episodic augmentation rather than structural underpinning.

7.2 Sell-through rate by region

Sell-through rates, a proxy for liquidity, reveal higher liquidity for Emin’s works in the U.S., where 94% of offered works cleared; however, transaction volume remains materially concentrated in the U.K., which accounted for 464 offered lots since 2018, compared to 95 in the U.S. The distinction suggests that while U.S. participation is highly effective, the U.K. functions as the primary transactional venue proving the market’s structural liquidity base.

Source: Artscapy | Visualisation: Darden Gildea

7.3 Geographical risk and institutional overlap

This concentration carries both stability and risk. The U.K. core provides continuity, but it also exposes the market to localised wealth cycles, currency dynamics, and regulatory conditions. A geographically diversified buyer base can buffer volatility; a domestically anchored one amplifies sensitivity to regional economic shifts.

The location of institutional validation therefore matters. The upcoming Tate Modern exhibition interacts directly with the market’s primary demand center. Rather than expanding Emin’s geographical reach, it reinforces an already dominant domestic base. By contrast, a major U.S. institutional retrospective could have introduced incremental cross-border absorption and potentially altered baseline pricing through geographical demand diversification.

In this context, the durability of an exhibition-driven repricing will depend less on symbolic canonisation and more on whether visibility meaningfully expands buyer geography beyond the U.K. core. Without that expansion, intensified competition remains locally concentrated rather than structurally transformative.

What the Tate changes

Beyond short-term liquidity effects, the Tate Modern retrospective represents a broader institutional recalibration. As Daniela Bianco observes, it signals “far more than an individual career milestone; it [marks] a structural shift in how major museums are rewriting the canon of post-war and contemporary art to fully integrate women artists into its core narrative rather than its margins.”

This framing situates the exhibition within a longer arc of canon consolidation. Institutional repositioning can influence how collectors interpret historical weight and long-term relevance. Whether such symbolic integration translates into durable repricing, however, depends on corresponding expansion in buyer depth rather than institutional validation alone.

8.1 Scenario 1: disciplined supply and concentrated competition

If upper-tier consignments remain selective during the anticipatory and exhibition phases, competitive intensity may compress around a narrow band of museum-scale paintings, neons, and major sculpture. In this configuration, liquidity tightens within dominant tiers while broader segments remain stable.

Under disciplined supply conditions, median expansion in the upper tier could hold through the exhibition window. The effect would manifest primarily in London, where domestic absorption capacity is strongest. Pricing strength in this scenario reflects temporary scarcity interacting with heightened institutional visibility.

Durability, however, would depend on whether high-calibre supply continues to be rationed beyond the exhibition period.

8.2 Scenario 2: deferred supply release and absorption ceiling

An alternative outcome emerges if consignors defer works into the exhibition window and then release material more broadly in the quarters that follow.

In this case, the market’s finite absorption capacity becomes binding. Incremental supply at mid- and upper-tier price bands could moderate pricing momentum as competitive intensity diffuses. Median stabilisation or softening would signal that buyer depth has not expanded proportionally to increased availability.

This scenario would not indicate structural weakness. It would reflect the market reverting to its established equilibrium once temporary visibility compression subsides.

8.3 Scenario 3: geographic broadening of demand

A more structural shift would require geographic diversification of buyer depth beyond the U.K. core. If the exhibition catalyses sustained cross-border participation — particularly from U.S. or Asian capital — incremental absorption capacity could widen.

Under this condition, supply expansion would encounter deeper demand bands, reducing sensitivity to marginal volume increases. Baseline pricing could stabilise at modestly elevated levels.

Historical precedent among comparable peers suggests this outcome is less probable absent international institutional anchoring. However, it remains the primary pathway through which Tate could influence long-term repricing dynamics.

8.4 Structural assessment

The exhibition therefore operates as a conditional catalyst. Its market impact will depend on the interaction between supply discipline, tier concentration, and geographic absorption.

Short-term competitive compression appears probable, but sustained repricing requires either constrained upper-tier supply or expanded buyer geography. Without one of these mechanisms, normalisation remains the baseline trajectory.

Strategic Pathways: positioning within a visibility cycle

9.1 Existing owners

For holders of museum-scale paintings, neons, and major sculpture, the exhibition may create a defined liquidity window during peak visibility. Owners considering disposition should evaluate timing carefully, particularly within the London market where demand concentration is strongest.

Post-exhibition supply expansion remains a key risk variable. Pricing firmness during the exhibition phase may moderate if deferred material re-enters the market.

Prints and Editions are unlikely to experience comparable repricing. Liquidity may remain stable, but expectations for catalyst-driven uplift should remain measured.

9.2 Prospective buyers