The hardest moment of owning art isn’t buying — it’s selling.

For most collectors, buying art feels intuitive. Emotional. Sometimes even joyful. Selling it, by contrast, is where complexity, opacity, and disappointment tend to concentrate. This asymmetry is not accidental. It sits at the very core of how the art market has evolved. Ownership is romanticised; acquisition is celebrated; discovery is mythologised. Exit, on the other hand, is ritualised, delayed, and deliberately obscured. Yet the moment a collector decides, or is forced, to sell is precisely when art stops being pure passion and becomes a test of market structure. To understand why selling art remains so difficult, we need to start much earlier: with the heterogeneous reasons people buy art, and the fragmented ways in which they enter the market.

Why we buy art: Many motives, one object

Art is one of the very few asset classes acquired for radically different reasons—often simultaneously, sometimes subconsciously. This diversity of intent is part of what makes art culturally powerful. It is also what makes the market structurally fragile at the moment of exit.

Decoration and aesthetic pleasure

For many collectors, art begins with a visceral response. A work resonates with a space. A colour, a form, or a gesture feels right. The artwork enters a home or an office not as an asset, but as part of an environment. These purchases are rarely framed in terms of resale. Over time, the work accumulates personal meaning. It becomes embedded in daily life, which makes the idea of selling feel distant—until it suddenly is not.

Trophy and status

Art has always functioned as a social signal. It communicates taste, access, and proximity to cultural power. Recognisable names, museum-backed artists, and historically validated works operate as shorthand. They confer legitimacy and status in a way few other assets can. In this context, price is often secondary to positioning.

Investment and wealth building

An increasing number of collectors buy art with explicit financial intent. They track artists across primary and secondary markets, study auction results, and think in terms of scarcity, career trajectories, and long-term appreciation. Art becomes part of a broader wealth strategy—albeit one without the infrastructure that traditional assets enjoy.

Philanthropy and patronage

Some collectors buy primarily to support artists and institutions. Their motivation is cultural rather than financial: enabling production, sustaining galleries, and contributing to artistic ecosystems. For these buyers, value is measured in impact, not multiples. Yet even here, market outcomes eventually matter—often unexpectedly.

Community and the practice of collecting

Collecting is also a social activity. A way of belonging to a network of peers, advisors, curators, and fellow enthusiasts. In this context, art is not just an object but a passport into a shared world. Transactions are embedded in relationships, which later complicates exit decisions.

The buying journey: Fluid, fragmented, and forgiving

Just as motivations vary, so do acquisition paths. The art market offers many ways in—and almost no standardised ways out.

Collectors may acquire works through:

- Walk-in galleries, openings, and art fairs, where relationships and access matter more than documentation

- Museums and exhibitions, where institutional validation shapes taste long before ownership

- Professional advisors, who add structure on the way in but often lack formalised exit frameworks

- Self-directed research, increasingly sophisticated but still constrained by incomplete data

- Friends, peers, and investor networks, where momentum travels socially

- Auctions, which provide public price signals without necessarily reflecting net outcomes

- Primary markets driven by narrative, and secondary markets driven by liquidity

- Moments of urgency, competition, or fear of missing out

Across these journeys, one feature consistently appears: prices are rarely upfront. Opacity is treated as tradition. Discovery is part of the ritual. Buyers accept this asymmetry because emotion, access, and urgency dominate the moment of acquisition. The problem is that this lack of transparency compounds over time.

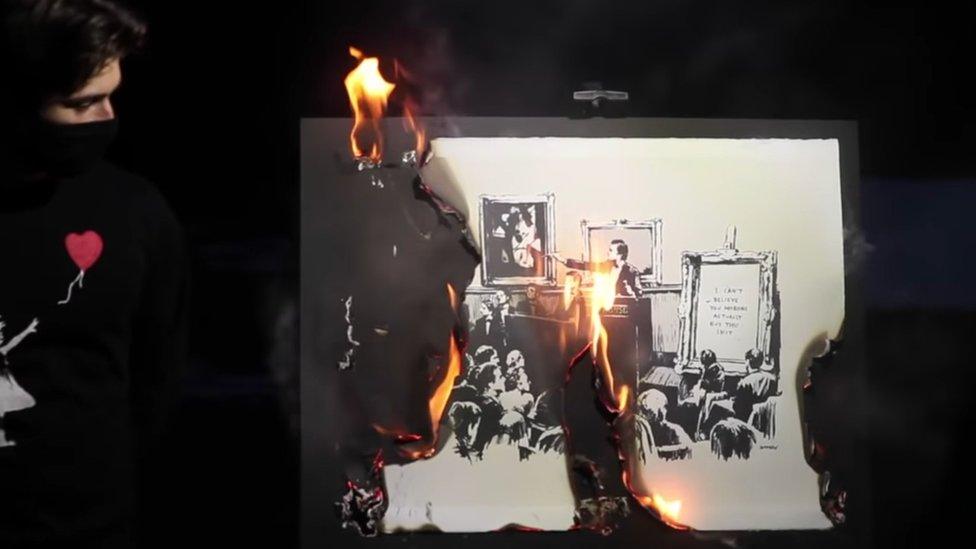

Banksy art burned in a video livestreamed from a park in New York. Photo: © Youtube

Where the system breaks: The moment of sale

Selling art exposes the structural limits of the market. When a collector decides to sell, they encounter a system optimised not for efficiency or fairness, but for discretion, delay, and discretionary pricing.

Auctions: Visibility without symmetry

Auctions are often perceived as the most transparent exit route. In reality, they are among the most asymmetric. Headline prices reflect what buyers pay, not what sellers receive. Between buyer’s premiums, seller’s commissions, marketing fees, and unfavourable terms, sellers routinely net 30–40% less than the public result suggests. The market celebrates the hammer price. The seller absorbs the friction.

Dealers and private sales

Private sales promise discretion, but operate on discretionary economics. Dealers apply spreads that commonly range from 30–50%, depending on urgency, relationships, and perceived leverage. Terms are bespoke. Timelines are elastic. Accountability is minimal. Advice is often persuasive rather than analytical.

Time as an undefined variable

Perhaps the most corrosive element is uncertainty. Weeks turn into months. Months drift into seasons. Sellers are rarely given clear expectations, milestones, or probabilities. Liquidity becomes a hope rather than a process.

Narrative over data

Most pricing guidance remains anecdotal. Comparables are selectively framed. Market momentum is described rhetorically rather than measured empirically. The seller is asked to trust expertise without being given visibility into its mechanics.

Artscapy: Bringing structure to the point of exit

Artscapy was built around a simple but radical idea: selling art should be as rigorous, data-driven, and transparent as any other financial decision.

AI-powered market estimates

Artscapy introduced the world’s first AI-powered art estimates which is: objective, continuously updated, and grounded in real transaction data. This creates a shared starting point. Not a promise, not a narrative, but a market-based reference. Try our art AI-estimate yourself and let us know what you think.

Speed as a function of process

Over 90% of consigned works sell in under 40 days, from consignment to client payout. This speed is not driven by pressure or discounting. It is the result of structured decision-making, accurate pricing, and correct channel selection.

Prestige-led, fully managed sales

Each artwork is positioned intentionally. Provenance, context, and placement are curated to maximise realised value. Execution is managed end-to-end, removing friction and guesswork for the collector.

Discretion by design

No work is made public unless explicitly agreed. We understand that an artwork can't be publicly hit the market. That's why Artscapy places works directly into other private collections, protecting both privacy and long-term price integrity.

Strategy before channel

Every sale begins with a recommendation on how and where to sell. If auction is deemed optimal, Artscapy selects the auction house most likely to deliver the best outcome for that specific artwork in that specific market moment—and negotiates favourable terms that waive seller fees typically imposed by auction houses.

From intuition to scientific rigour

Artscapy replaces intuition with methodology. Accuracy of data, repeatable processes, and scalability transform selling from an art into a discipline. A team of experienced art professionals assists our clients from the first moment until the work is safely placed in a new house.

Avoiding the risk of “burning” a work

In art markets, to “burn” a work means to expose it unsuccessfully—publicly offering it at a price the market refuses. Once burned, a work carries stigma. Future buyers anchor to failure. Liquidity dries up. Value erosion can persist for years. By aligning pricing, timing, and channel before exposure, Artscapy eliminates this risk.

Rethinking ownership

Buying art is easy because it is driven by desire. Selling art is hard because it reveals structure, or the lack of it. If art is to be treated seriously as part of modern wealth, the moment of exit must evolve. Artscapy exists to make that evolution possible: turning the most complicated moment of owning art into a process defined by clarity, discipline, and trust.

Collectors today expect the same clarity, tooling, and autonomy they experience in other areas of their financial lives. They want to understand what they own, what it’s worth today, and how that value behaves over time — without pressure, without hype, and without having to decode an opaque system.

This is where Artscapy’s AI Estimates fit in.